Am I eligible to apply for a

Habitat Home?

Determine if you are eligible to apply for a Habitat Home.

If you meet our three prerequisites below, you are eligible to apply for homeownership with Teton Habitat.

01

What is your U.S. Residency Status?

If you are a US Citizen, Lawful Permanent Resident, or a DACA Recipient with a valid Social Security number and Employment Authorization Document, you are eligible to apply.

02

Do you currently own or have you owned real estate in the last three years?

If you do not own or have owned real estate in the last three years, you are eligible to apply.

03

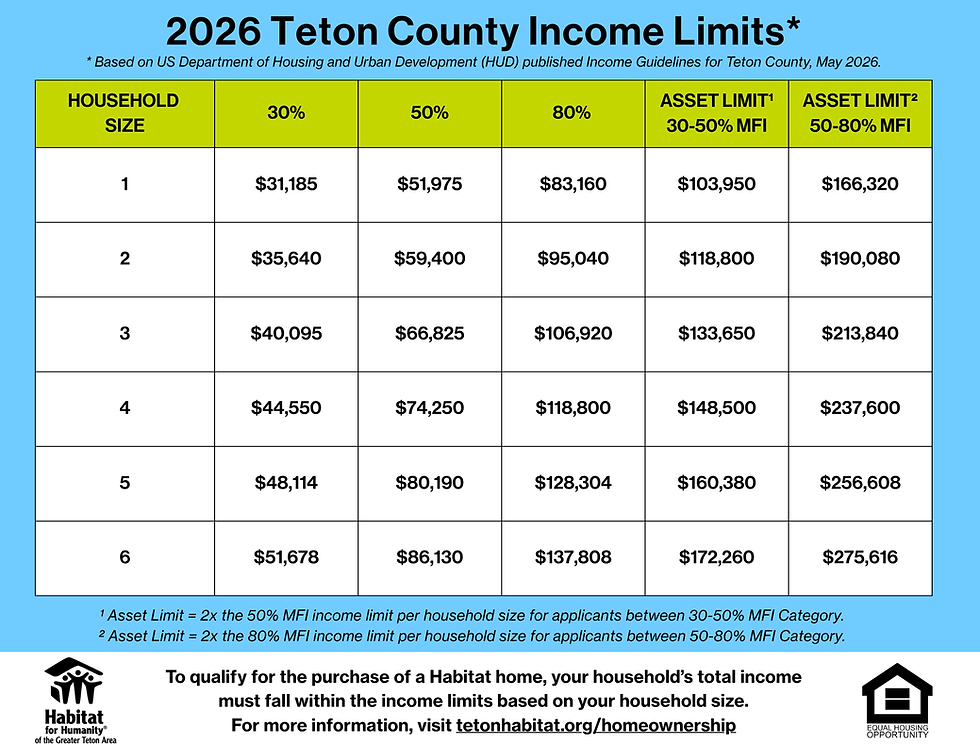

What is your annual household income?

Your annual household income is the pre-tax total salary of all the earners in your household. Check the Income Range Guidelines Chart below to see if you are eligible to apply, and click the arrow to the right to learn more information about your income range.

For example, a family of four has two full-time working parents, an 18 year old working part-time, and 12 year old. The three of them earn $100,000 annually, so they fall within the income range for a 4 person household.

These income ranges are based on the U.S. Department of Housing and Urban Development (HUD) income guidelines for Teton County, Wyoming in May, 2026. Income ranges are updated on a yearly basis.

2026 Annual Income Ranges

30% - 80% MFI

How do I purchase a Habitat Home?

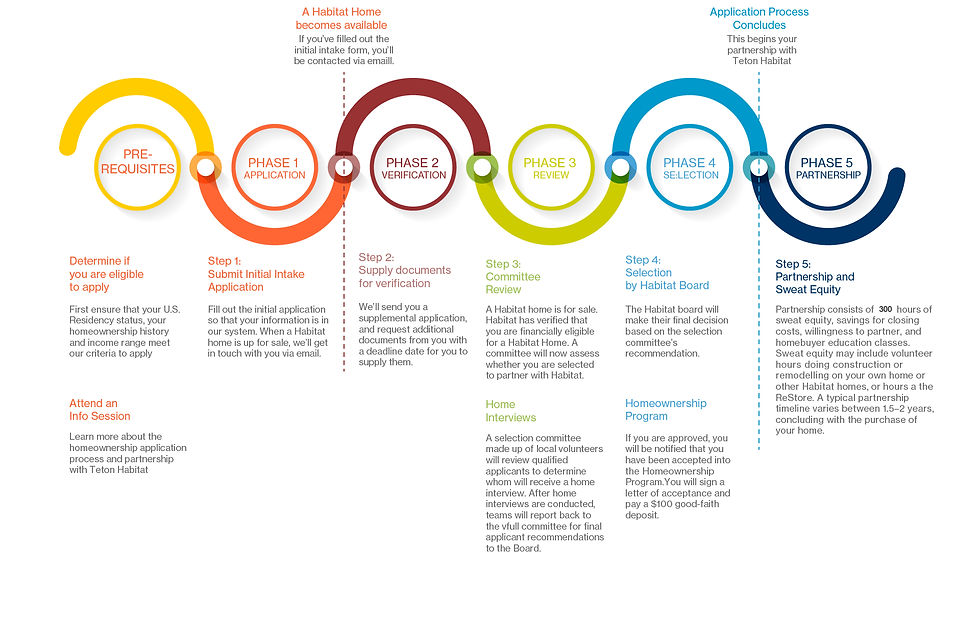

Now that you have determined that you are eligible to apply, read more below to learn about The Habitat Homeowner application process and path to homeownership. This process may take 18–24 months to complete.

Application Process Overview

STEP 1

FILL OUT YOUR

INITIAL INTAKE FORM

Now that you know that you meet the three prerequisites to apply for a Habitat Home, you’ll need to enter your information into the Habitat system. We accept initial intake forms year-round. The initial intake form is NOT AN APPLICATION. When a new home comes up for sale, you will be notified with a deadline of when to submit your financial documents for verification. Please ensure you have a recent and valid email address; you will be notified via email.

Waiting Period

Now that you know that you meet the three prerequisites to apply for a Habitat Home, and you have entered your intake form into the Habitat system, you will be notified via email when a Habitat Home comes up for sale.

UNTIL WE HAVE A UNIT

AVAILABLE FOR PURCHASE

STEP 2

SUPPLY YOUR FINANCIAL INFORMATION FOR VERIFICATION

You have determined that you meet the three prerequisites to apply for a Habitat Home and your initial intake form information is in the system. When a Habitat home becomes available, we will contact you via email. We will then request documents and information to verify that you are financially eligible for a Habitat Home.

STEP 3

INTERVIEW FOR

COMMITTEE REVIEW

After Habitat reviews income verification documents for financial eligibility, qualifying applicants will move onto the review phase. A selection committee made up of local volunteers will review the qualified applicants to determine whom will receive a home interview. If you are selected for a home interview, you will be contacted by a team of selection committee members for potential dates and times. After home interviews are conducted, teams will report back to the full committee for final applicant recommendations to the Board. The Habitat board will make their final decision based on the selection committee’s recommendation.

STEP 4

SELECTION

The committee has recommended you to the Habitat Board. If you are approved, you will be notified that you have been accepted into the Homeownership Program. You will sign a letter of acceptance and pay a $100 good-faith deposit. This ends the application process, and begins your partnership with Habitat. Partnership consists of 300 hours of sweat equity, savings for closing costs, willingness to partner, and homebuyer education classes. Sweat equity can be building or remodeling your own home, volunteering to build other Habitat Homes, or at the ReStore. The typical partnership timeline varies between one and a half to two years.

Path to Homeownership

This process may take 18–24 months to complete.

Additional Resources

Teton County Affordable Housing Agencies

(Sales and Rental)

If you do not qualify for a Habitat home, we encourage you

to check out other affordable housing resources in Teton County.

110 E Broadway, 2nd floor

P.O. Box 4498

Jackson, WY 83001

307.739.0665

Jackson/Teton County Affordable Housing Department

320 S. King Street

P.O. Box 714

Jackson, WY 83001

307.732.0867